Accounting principles and procedures

| Question | Answer |

|---|---|

| What is Accounting? | Accounting is the art of recording, summarizing, reporting, and analyzing financial transactions. It can be a complete record of all the activities of a business, providing details of every aspect of the business, allowing the analysis of business trends, and providing insight into future prospects. |

| Why does a business keep company accounts? | Company accounts are required in order to:- Record and measure a company’s profitability. For tax calculation purposes including calculating taxable deductions. Legislation requires companies to keep accurate records. Business Growth is encouraged by identifying profitable operations whilst also allowing management to minimise any loss making activities. |

| What are the types of accounting? | Financial accounting. … Public accounting. … Government accounting. … Forensic accounting. … Management accounting. … Tax accounting. … Internal auditing. |

| What is Financial Accounting? | Financial Accounting, or financial reporting, is the process of producing information for external use usually in the form of financial statements. Financial Statements reflect an entity’s past performance and current position based on a set of standards and guidelines known as GAAP (Generally Accepted Accounting Principles). |

| What is Management Accounting? | Management accounting is a branch of accounting that focuses on the revenues and expenses of a business, as well as asset usage. Someone engaged in management accounting notes unusual spikes and declines in revenues and expenses, and reports these variances to management. The intent of this analysis is to take action to improve the financial performance of a business. Management accounting results in reports that are intended for use within a business. Since this information is not viewed by outsiders, it does not have to comply with the reporting requirements of any accounting frameworks, such as generally accepted accounting principles. Instead, the accounting staff can generate reports in any format they want, in order to highlight actionable information. |

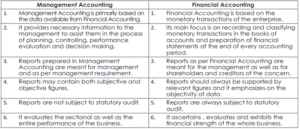

| What is difference between Financial Accounting & Management Accounting? |  |

| What is Cost Accounting? | Cost accounting is a branch of management accounting and involves the application of various techniques to monitor and control costs. Its application is more suited to manufacturing / Construction business |

| What are the steps/phases of an Accounting cycle? | a) Recording of Transaction:- As soon as a transaction happens it is at first recorded in subsidiary books. b) Journal :- The transactions are recorded in Journal chronologically. c) Ledger:- All journals are posted into ledger chronologically and in a classified manner. d) Trial Balance:- After taking all the ledger account closing balances, a Trial Balance is prepared at the end of the period for the preparation of financial statements. e) Adjustment Entries :- All the adjustments entries are to be recorded properly and adjusted accordingly before preparing financial statements. f) Adjusted Trial Balance:- An adjusted Trial Balance may also be prepared. g) Closing Entries:- All the nominal accounts are to be closed by transferring to Trading Account and Profit and Loss Account. h) Financial Statements:- Financial statement can now be easily prepared which will exhibit the true financial position and operating results. |

| Definition of Journal. | Journal is a book where the information from source documents is first recorded. It is also known as book of original entry. Journal is a book of prime entry in which transactions are copied in order of date. The entries as they are copied, are classified into debits and credits, so as to facilitate them being correctly posted afterwards in the ledger. |

| Definition of Ledger. | A ledger is an accounting book that facilitates the transfer of all journal entries in a chronological sequence to individual accounts. The process of recording journal entries into the ledger is called posting. |

| What are the Qualitative Characteristics of Accounting Information? | (i) Reliability (ii) Relevance (iii) Materiality (iv) Understandability (v) Comparability |

| Definition of Transaction. | Transaction: It means an event or a business activity which involves exchange of money or money’s worth between parties. The event can be measured in terms of money and changes the financial position of a person e.g. purchase of goods would involve receiving material and making payment or creating an obligation to pay to the supplier at a future date. Transaction could be a cash transaction or credit transaction. When the parties settle the transaction immediately by making payment in cash or by cheque, it is called a cash transaction. In credit transaction, the payment is settled at a future date as per agreement between the parties. |

| Definition of Asset. | Asset: Asset is a resource owned by the business with the purpose of using it for generating future profits. |

| What are the Types of Assets? | Assets can be Tangible and Intangible. Tangible Assets are the Capital assets which have some physical existence. They can, therefore, be seen, touched and felt, e.g. Plant and Machinery, Furniture and Fittings, Land and Buildings, Books, Computers, Vehicles, etc. The capital assets which have no physical existence and whose value is limited by the rights and anticipated benefits that possession confers upon the owner are known as lntangible Assets. They cannot be seen or felt although they help to generate revenue in future, e.g. Goodwill, Patents, Trade-marks, Copyrights, Brand Equity, Designs, Intellectual Property, etc. Assets can also be classified into Current Assets and Non-Current Assets. Current Assets – An asset shall be classified as Current when it satisfies any of the following : (a) It is expected to be realised in, or is intended for sale or consumption in the Company’s normal Operating Cycle, (b) It is held primarily for the purpose of being traded , (c) It is due to be realised within 12 months after the Reporting Date, or (d) It is Cash or Cash Equivalent unless it is restricted from being exchanged or used to settle a Liability for at least 12 months after the Reporting Date. Non-Current Assets – All other Assets shall be classifi ed as Non-Current Assets. e.g. Machinery held for long term etc. |

| What is the difference between a current asset vs. a fixed asset? | Current assets can normally be converted into cash within one financial year and are regarded as assets that allow day to day operation of the business. Examples may include money owed to the company following sales of its products or services, inventory and prepaid expenses. Fixed assets typically cannot be converted into cash within one year. These kinds of assets are recorded on a company’s balance sheet as fixed assets the company owns on a long term basis. Examples include vehicles, office furniture, machinery, buildings and land. |

| Definition of Liability. | Liability: It is an obligation of financial nature to be settled at a future date. It represents amount of money that the business owes to the other parties. E.g. when goods are bought on credit, the firm will create an obligation to pay to the supplier the price of goods on an agreed future date or when a loan is taken from bank, an obligation to pay interest and principal amount is created. |

| What are the Types of Liability? | Depending upon the period of holding, these obligations could be further classified into Long Term or non-current liabilities and Short Term or current liabilities. Current Liabilities – A liability shall be classified as Current when it satisfies any of the following : (a) It is expected to be settled in the Company’s normal Operating Cycle, (b) It is held primarily for the purpose of being traded, (c) It is due to be settled within 12 months after the Reporting Date, or (d) The Company does not have an unconditional right to defer settlement of the liability for at least 12 months after the reporting date (Terms of a Liability that could, at the option of the counterparty, result in its settlement by the issue of Equity Instruments do not affect its classification) Non-Current Liabilities – All other Liabilities shall be classified as Non-Current Liabilities. E.g. Loan taken for 5 years, Debentures issued etc. |

| Definition of Internal Liability. | Internal Liability : These represent proprietor’s equity, i.e. all those amount which are entitled to the proprietor, e.g., Capital, Reserves, Undistributed Profits, etc. |

| Definition of Working Capital. | Working Capital : In order to maintain flows of revenue from operation, every firm needs certain amount of current assets. For example, cash is required either to pay for expenses or to meet obligation for service received or goods purchased, etc. by a firm. On identical reason, inventories are required to provide the link between production and sale. Similarly, Accounts Receivable generate when goods are sold on credit. Cash, Bank, Debtors, Bills Receivable, Closing Stock, Prepayments etc. represent current assets of firm. The whole of these current assets form the working capital of a firm which is termed as Gross Working Capital. Gross Working capital = Total Current Assets Working Capital (Net) = Current Assets – Currents Liabilities. |

| What are financial statements? What are the key financial statements that all companies must provide? | Financial statements are reports businesses compile to record the company’s financial performance and health. They offer a clear, standardized picture to stakeholders like investors, creditors, and management to see how well the business operates and assess whether it’s headed in the right direction. 1. Profit & Loss accounts – the incomes and expenditures of a company and the resulting profit or loss. 2. Balance Sheets – the companies assets and liabilities. 3. Cash flow statements – a statement summarising the company’s cash inflows and outflows over a specific period of time. 4. Changes to the Equity – A statement of changes in equity summarizes the movement in the equity accounts during the year namely share capital, share premium, retained earnings, revaluation surplus, unrealized gains on investments, etc. |

| What is a Profit and Loss Account? | Profit and Loss Account or Income Statement : This account shows the revenue earned by the business and the expenses incurred by the business to earn that revenue. This is prepared usually for a particular accounting period, which could be a month, quarter, a half year or a year. The net result of the Profit and Loss Account will show profit earned or loss suffered by the business entity. |

| What are Balance Sheets? | Balance Sheet : It is the statement of financial position of the business entity on a particular date. It lists all assets, liabilities and capital. It is important to note that this statement exhibits the state of affairs of the business as on a particular date only. It describes what the business owns and what the business owes to outsiders (this denotes liabilities) and to the owners (this denotes capital). It is prepared after incorporating the resulting profit/losses of Income statement. |

| What is the difference between a profit and loss account and a balance sheet? | A profit and loss account shows the incomes and expenditures of a company and the resulting profit or loss. The balance sheet shows what a company owns (its assets) and what it owes (its liabilities) at a given point in time. |

| What is GAAP? | Generally accepted accounting principles (GAAP) are a common set of accounting principles, standards and procedures that companies must follow when they compile their financial statements. GAAP is a combination of authoritative standards (set by policy boards) and the commonly accepted ways of recording and reporting accounting information. GAAP improves the clarity of the communication of financial information. GAAP is only used in the United States. |

| What is IFRS? | IFRS is short for International Financial Reporting Standards. IFRS is the international accounting framework within which to properly organize and report financial information. It is derived from the pronouncements of the London-based International Accounting Standards Board (IASB). It is currently the required accounting framework in more than 120 countries. It requires businesses to report their financial results and financial position using the same rules; this means that, barring any fraudulent manipulation, there is considerable uniformity in the financial reporting of all businesses using IFRS, which makes it easier to compare and contrast their financial results. IFRS is used in more than 110 countries around the world, including the EU and many Asian and South American countries. |

| What are the Basic Assumptions in Accounting? | 1. Business Entity Concept – As per this concept, the business is treated as distinct and separate from the individuals who own or manage it. 2. Going Concern Concept – The basic principles of this concept is that business is assumed to exist for an indefinite period and is not established with the objective of closing it down. 3. Money Measurement Concept – A business transaction will always be recorded if it can be expressed in terms of money. 4. Accounting Period Concept – the business entity is supposed to be paused after a certain time interval. This time interval is called an accounting period. This period is usually one year, which could be a calendar year i.e. 1st January to 31st December or it could be a fiscal year in India as 1st April to 31st March. 5. Accrual Concept – The accrual concept is based on recognition of both cash and credit transactions. In case of a cash transaction, owner’s equity is instantly affected as cash is either received or paid. In a credit transaction, however, a mere obligation towards or by the business is created. |

| What are the Basic Principles of Accounting? | 1. Revenue Realization Concept – It says amount should be recognized only to the tune of which it is certainly realizable. Thus, mere getting an order from the customer won’t make it eligible to recognize as revenue. The reasonable certainty of realizing the money will come only when the goods ordered are actually supplied to the customer and he is billed. This concept ensures that income unearned or unrealized will not be considered as revenue and the firms will not inflate profits. 2. Matching Concept – when a given event has two effects – one on revenue and the other on expense, both must be recognized in the same accounting period. 3. Full Disclosure Concept – As per this concept, all significant information must be disclosed 4. Dual Aspect Concept – it is the foundation of double-entry accounting, which requires that every transaction affect two accounts in equal and opposite ways. For instance, purchasing equipment for cash increases the asset account (equipment) and decreases another asset account (cash). 5. Verifiable Objective Evidence Concept – Under this principle, accounting data must be verified. In other words, documentary evidence of transactions must be made which are capable of verification by an independent expert. 6. Historical Cost Concept – Business transactions are always recorded at the actual cost at which they are actually undertaken. 7. Balance Sheet Equation Concept – Under this principle, all which has been received by us must be equal to that has been given by us and needless to say that receipts are clarified as debits and giving is clarified as credits. The basic equation,appears as :- Debit = Credit |

| What are the Modifying Principles of Accounting? | 1. Materiality Concept – This is more of a convention than a concept. It proposes that while accounting for various transactions, only those which may have material effect on profitability or financial status of the business should have special consideration for reporting. What this convention claims is to attach importance to material details and insignificant details should be ignored while deciding certain accounting treatment. The concept of materiality is subjective and an accountant will have to decide on merit of each case. Generally, the effect is said to be material, if the knowledge of an event would influence the decision of an informed stakeholder. 2. Consistency Concept – This concept advocates that once an organization decides to adopt a particular method of revenue or expense recognition in line with the other concepts, the same should be consistently applied year after year, unless there is a valid reason for change in the method. 3. Conservatism Concept – The concept underlines the prudence of under-stating than over-stating the net income of an entity for a period and the net assets as on a particular date. This is because business is done in situations of uncertainty. For years, this concept was meant to “anticipate no profits but recognize all losses”. This can be stated as (i) Delay in recognizing income unless one is reasonably sure (ii) Immediately recognize expenses when reasonably sure 4. Timeliness Concept – Under this principle, every transaction must be recorded in proper time. 5. Industry Practice Concept – The accounting practice which has always prevailed in the industry is followed by it. |

| What are the types of Accounts? | (1) Personal Account : As the name suggests these are accounts related to persons. (a) These persons could be natural persons like Suresh’s A/c, Anil’s a/c, Rani’s A/c etc. (b) The persons could also be artificial persons like companies, bodies corporate or association of persons or partnerships etc. Accordingly, we could have Videocon Industries A/c, Infosys Technologies A/c, Charitable Trust A/c, Ali and Sons trading A/c, ABC Bank A/c, etc. (c) There could be representative personal accounts as well. Although the individual identity of persons related to these is known, the convention is to reflect them as collective accounts. e.g. when salary is payable to employees, we know how much is payable to each of them, but collectively the account is called as ‘Salary Payable A/c’. Similar examples are rent payable, Insurance prepaid, commission pre-received etc. The students should be careful to have clarity on this type and the chances of error are more here. (2) Real Accounts : These are accounts related to assets or properties or possessions. Depending on their physical existence or otherwise, they are further classified as follows:- (a) Tangible Real Account – Assets that have physical existence and can be seen, and touched. e.g. Machinery A/c, Stock A/c, Cash A/c, Vehicle A/c, and the like. (b) Intangible Real Account – These represent possession of properties that have no physical existence but can be measured in terms of money and have value attached to them. e.g. Goodwill A/c, Trade mark A/c, Patents & Copy Rights A/c, Intellectual Property Rights A/c and the like. (3) Nominal Account : These accounts are related to expenses or losses and incomes or gains e.g. Salary and Wages A/c, Rent of Rates A/c, Travelling Expenses A/c, Commission received A/c, Loss by fire A/c etc. |

| What is the double-entry bookkeeping system? | A double-entry bookkeeping system is a set of rules for recording financial information in a financial accounting system in which every transaction or event changes at least two different nominal ledger accounts. In the double entry system, transactions are recorded in terms of debits and credits. Since a debit in one account will be offset by a credit in another account, the sum of all debits must therefore be exactly equal to the sum of all credits. The double-entry system of bookkeeping or accounting makes it easier to accurately prepare financial statements directly from the books of account and detect errors. |

| What is the basic Accounting equation? | Assets = Liabilities + Owner’s equity |

| What are Capital Expenses? | Capital expenditure includes costs incurred on the acquisition of a fixed asset and any subsequent expenditure that increases the earning capacity of an existing fixed asset. Capital Expenditure may include the following: Purchase costs (less any discount received), Delivery costs, Legal charges, Installation costs, Upgradation costs, Replacement costs |

| What are Revenue Expenses? | Revenue expenditure incurred on fixed assets include costs that are aimed at ‘maintaining’ rather than enhancing the earning capacity of the assets. These are costs that are incurred on a regular basis and the benefit from these costs is obtained over a relatively short period of time. Revenue costs therefore comprise of the following: Repair costs, Maintenance charges, Repainting costs, Renewal expenses |

| What are the notes to the accounts? | Notes to the financial statement present all such information which cannot be presented on the face of income statement, balance sheet, statement of cash flows and statement of changes in equity. |

| What is an Audit ? | An unbiased, An independent assessment ,examination and evaluation of the financial statements of an organization. It can be done internally (by employees of the organization) or externally (by an outside firm). |

| What is the Purpose of the Audit? | Check the adherence to the Accounting standards Check for Frauds, Manipulations, Conflicts of interests etc. Build up shareholders/stakeholders confidence about the business |

| Please explain your understanding of the term tax depreciation? | Tax depreciation is where the declining value of an asset is offset against a companies taxable profit. The depreciation in value can be recorded as an expense in order to reduce the amount of taxable income. This can be applied on things such as plant, tools, vehicles, computers, furniture and buildings. |

| What are overheads? | The terms overheads refers to the operating cost of the business that are incurred on an ongoing basis. Overheads can be both fixed or variable for example:- Fixed overheads could take the form of rent on office buildings or building insurance costs that do not change each month. Variable overheads tend to fluctuate depending on the activity of the business for example delivery or utility charges. |

| Please explain your understanding of Project Bank Accounts? | A Project Bank Account (PBA) is a dedicated, ring-fenced bank account used in construction projects to manage payments securely and transparently. It is designed to ensure that all parties involved in a project including subcontractors, suppliers, and the main contractor receive payments directly and promptly from the account, minimising the risk of late or non-payment. A PBA is set up at the start of a construction project, with agreements in place between the employer, main contractor, and participating subcontractors on how payments are made. The employer deposits funds into the PBA for work completed with payments then made simultaneously to all parties listed in the PBA agreement based on pre-agreed terms which bypasses the traditional hierarchical payment flows from Client to Main Contractor down to supply chain level. |

| What is an escrow account? | Escrow accounts are contractual agreements that are used as financial instruments within a transaction. The asset or currency being transferred between two primary parties is held by an intermediary third party. The currency being exchanged is held securely by the third party until each of the 2 parties have met their contractual obligations allowing the money to then be transferred. This is often used by mortgage lenders when completing on the buying or selling of the real estate being exchanged. |

| What is Ratio analysis? Please name the three different types of accounting ratios? | Ratio analysis is calculating several financial ratios from a company’s financial statements and using them to evaluate its financial standing. The three different types of accounting ratios are made up of:- 1. Liquidity ratios which consider an organisations ability to pay their debt obligations and assess its margin of safety by looking at a number of metrics including their operating cash against short term debts. 2. Profitability ratios assess an organisations ability to generate profits from its sales operations and shareholding equity. The ratio indicates how efficient a company is in generating its profit. 3. Gearing ratios compare capital within the company against its debts. The gearing is a measure of a companies financial leverage and sets out what proportion of the firms activities are funded by shareholders vs its creditor funds. |

| What is financial leverage? | Financial leverage is the concept of using borrowed funds in the form of debt to enhance business operations and increase the companies profitability and rates of return. In the event that the rate of return invested via borrowed funds is higher than the interest on those funds then more profit can be generated. |

| What is ‘Return On Capital Employed (ROCE)’? | Return on capital employed (ROCE) is a financial ratio that measures a company’s profitability and the efficiency with which its capital is employed. ROCE is calculated as: ROCE = Earnings Before Interest and Tax (EBIT) / Capital Employed |

| Why do chartered surveyors in your pathway need to understand and be able to interpret company accounts? | ◦For your own business accounts. ◦For assessing the covenant strength of potential tenants and landlords. ◦For assessing the financial strength of contractors and those tendering for contracts. ◦For profits-method valuations (for leisure properties). ◦For assessing competition. |

| What documents will you check in Pre-Qualification of Contractors? | Financial statements, Financial ratios, Cashflow on other projects |

| What is a Notional final account? | A Notional Account in construction contract is a Final Account prepared for projects facing insolvency, or for project contracts that are to be determined except by performance. It is sometimes referred to as Notional Final Account, i.e anticipated or projected final account for project that has to be determined (terminated) but yet to be completed. |

| What’s the difference between a bank guarantee and a letter of credit? | Letters of credit ensure that a transaction proceeds as planned, while bank guarantees reduce the loss if the transaction doesn’t go as planned. A letter of credit is an obligation taken on by a bank to make a payment once certain criteria are met. Once these terms are completed and confirmed, the bank will transfer the funds. The letter of credit ensures the payment will be made as long as the services are performed. A bank guarantee, like a letter of credit, guarantees a sum of money to a beneficiary. Unlike a letter of credit, the sum is only paid if the opposing party does not fulfill the stipulated obligations under the contract. This can be used to essentially insure a buyer or seller from loss or damage due to nonperformance by the other party in a contract. |

| What is dividend yield? | The dividend yield shows how much a company has paid out in dividends over the course of a year. The yield is presented as a percentage, not as an actual dollar amount. This makes it easier to see how much return per dollar invested the shareholder receives through dividends. The yield is calculated as follows: Annual Dividends per Share / Price per Share. |

| What is dividend cover? | Dividend cover is the ratio of company’s net income over the dividend paid to shareholders, calculated as earnings per share divided by the dividend per share. It helps indicate how sustainable a dividend is. Dividend Cover of less than 1.5 may indicate a danger of a dividend cut while more than 2 is viewed as healthy. The inverse of dividend cover is the Payout Ratio. |

| What is the difference between GAAP & IFRS? | 1. Rule-based vs principle-based – IFRS is built on principles and it gives businesses a set of rules to adhere to when they present their financial statements. Rather than only considering a transaction or event’s legal form, IFRS concentrates on its content. GAAP is rule-based, meaning that it stipulates particular guidelines and instructions that businesses must adhere to while creating their financial statements. Instead of emphasising the content of transactions, it concentrates on their legal form. 2. Inventory handling – IFRS expressly forbids the use of the LIFO approach and only permits FIFO. IFRS does not accept this practice because it is impossible to establish proper inventory flow with LIFO. This could lead to an incorrect income figure that does not accurately depict the situation. If you’re utilising GAAP, you can determine inventory using the FIFO (First in, First out) or LIFO (Last in, First out) technique. Organisations are free to select the most practical way, thanks to the GAAP standard. 3. Asset identification – The definition of assets under IFRS is broader, enabling businesses to account for intangible assets like goodwill, trademarks and patents. GAAP has a more stringent definition of assets, allowing only physical assets, including buildings, land and machinery, to be recognised. 4. Write downs – The IFRS permits the value of an asset to be reversed when its price rises. GAAP regulations mandate that businesses write down the value of fixed or inventory assets; once written down, the asset’s market value cannot be recovered, even if it rises over time. As a result, contrary to IFRS, the GAAP regulation may result in inaccuracies because it doesn’t account for increases in asset market value. |

| Why GAAP is not used in Middle East? | UAE has emerged as a global financial center. By adopting IFRS, the UAE aligned its practices with global standards, ensuring its businesses remained competitive and appealing to foreign investors. In contrast to countries with established national GAAP frameworks, the UAE does not maintain a distinct Generally Accepted Accounting Principles (GAAP) standard. Instead, companies operating in the UAE align with IFRS, which functions as the de facto standard. Historically, the UAE’s regulatory environment has emphasized compliance with internationally recognized frameworks, negating the need for a separate GAAP system. |

| What are intangible assets? | An intangible asset is defined under International Financial Reporting Standards (IFRS®) as ‘an identifiable, non-monetary asset without physical substance’. e.g. patent, brand, trademark, or copyright |

| How do you determine the value of an intangible asset? | Intangible assets are initially measured at cost. The cost of an intangible asset comprises: 1. Acquisition cost: If the asset is purchased separately, its cost includes the purchase price, import duties and non-refundable taxes after deducting trade discounts. 2. Internally developed assets: For internally developed assets, the cost includes all directly attributable costs necessary to create, produce and prepare the asset for its intended use, such as materials, labour and overhead. The key issue in measuring internally developed assets is how to identify which costs should be capitalised and how these can be supported by sufficient, appropriate audit evidence. Development costs tend to be mostly staff time which is supported by contracts and timesheets. Management must apply judgement in considering whose time and the quantum of costs to capitalise. Management must consider whether staff activity and the relevant costs are directly attributable to the intangible asset. 3. Acquisition as part of business combination: If an intangible asset is acquired in a business combination, its cost is recognised at fair value at the acquisition date. After initial recognition, an entity must choose between two models for subsequent measurement: 1. Cost model – The asset is carried at cost less any accumulated amortisation and impairment losses 2. Revaluation model – Intangible assets can be carried at revalued amounts (fair value) less any subsequent amortisation and impairment losses |

| Under what circumstances, an escrow account is required for a Project? | The escrow account law applies to all real estate developers working in Dubai and those who sell units off-plan, and, in return, receive payments from purchasers or investors as well as from the financiers of the project. |

| What is Standby Letter of Credit? | If a transaction fails and one party is not compensated as it should have been, the standby letter is payable when the beneficiary can prove it did not receive what was promised. This is used more as insurance and less as a means of facilitating an exchange. They are commonly used in various scenarios, including construction projects, international trade, and commercial transactions. |

| What is Irrevocable Letter of Credit? | It cannot be modified or revoked without the agreement of all parties involved, offering a high level of security for both the buyer and the seller. |

| What is a Confirmed Letter of Credit? | A confirmed letter of credit involves the addition of a confirmation by a bank other than the issuing bank, typically the seller’s bank. This confirmation serves as a secondary guarantee of payment. This adds an extra layer of security for the seller. The seller can rely not only on the issuing bank’s credit but also on the assurance of payment from the confirming bank. This type might be most suitable usually when the beneficiary does not trust the other party’s bank. |

| What is a Revolving Letter of Credit? | A revolving letter of credit is used for multiple shipments over a specified period, allowing the buyer to make multiple drawdowns up to a predetermined limit. This type of letter is useful for ongoing business relationships where there are frequent transactions between the buyer and the seller. It is continually replenished as it is drawn by the beneficiary. |

| What is difference between Insolvency and Bankruptcy? | Insolvency is a financial state in which a person cannot meet debt payments on time. It’s not having enough money to meet your obligations. Bankruptcy is a legal process that happens when a person declares he or she can no longer pay back his or her debts to creditors. It’s a solution when you don’t have enough money to meet your obligations. In essence, the state of insolvency can lead you to declare bankruptcy. However, insolvency does not necessarily lead to bankruptcy. |

| What is Acid test ratio? | The acid test ratio indicates whether a company has the ability to pay its short-term obligations. The acid-test ratio, commonly known as the quick ratio, uses data from a firm’s balance sheet to indicate whether it has the means to cover its short-term liabilities. Generally, a ratio of 1.0 or more indicates a company can pay its short-term obligations, while a ratio of less than 1.0 indicates it might struggle to pay them. |

| What is difference between Price Fluctuation and Price Escalation? | Price escalation refers to the increase in prices of goods or services over a period. Price Variation is less predictable, prices going up and down. |

| What is credit control? How is relevant Credit Control to your work? | Credit control processes help you ensure your company’s payment terms and policies are respected. This involves making your credit policies clear to both your customers and your credit control team: explain how you’ll issue invoices, and what you’ll do if they go past due. |

| What is direct tax? Is VAT direct or indirect tax? | Direct taxes are levied on individuals or entities directly by the government. In contrast, Indirect taxes are those collected by an intermediary (e.g. marketplaces, manufacturers, platform owners, vendors) from the end consumer. In other words, the direct tax burden falls directly on the taxpayer, whereas indirect taxes are paid by consumers indirectly through the goods and services they purchase. If they are imposed only on the final supply to a consumer, they are direct. They are indirect if they are imposed as value-added taxes (VATs) along the production process. |

| What are the functions of Accounting? | The main functions of accounting are analyzing financial data, preparing budgets, cost control, detecting and mitigating risks, accounts payable and receivable, payroll, reporting financial analysis, compliance and tax audits, and determining profitability, liquidity, and solvency |

| Who is an Accountant? | Accountants are financial professionals employed by accounting firms or in the accounting departments of large companies. Their roles include monitoring of a company’s or individual’s income, expenditures, and liabilities. Tax preparation and tax planning are specialized roles for accountants. |

| Who is a Chartered Accountant? | A chartered accountant (CA) is a financial professional qualified to execute certain accounting procedures. It also refers to an accounting designation granted internationally to individuals, in countries outside of the United States. This designation is the same as the certified public accountant (CPA) designation in the United States. CAs work in four main areas: applied finance, financial accounting and reporting, management accounting, and taxation. Their responsibilities may include filing taxes and auditing financial statements. CAs are more highly qualified and experienced, and will be a member of a professional body such as Emirates Association for Accountants & Auditors (EAAA) |

| What is importance of Accounting Principles? | Accounting principles help standardize accounting methods, ensuring that financial information is consistent and comparable across different periods and entities. |

| What are three methods for inventory valuation? | FIFO (First In, First Out), LIFO (Last In, First Out), WAC (Weighted Average Cost) |

| What is Weighted Average Method? | Weighted average cost accounting calculates the average cost of all inventory units available for sale over a respective period, which is then used to determine the cost of goods sold and the value of ending inventory. |

| What are Bad debts? | a debt that cannot be recovered. |

| What Is Paid-Up Capital? | Paid-up capital is the amount of money that the company gains by selling its shares and not the money that is borrowed. So the paid-up capital represents the company’s current status and how dependent the company is on the shares and how easily the company can pay off its debts. |

| What is Single entry system? | Single-entry accounting (also known as single-entry bookkeeping) is a method of tracking a company’s assets, liabilities, income, and expenses by recording each transaction one single time. As its name suggests, it lists income and expenses in a single row, with positive values for income and negative values for expenses. When a business sells a good using single-entry accounting, the expenses for the good are recorded when the business purchases the good and the revenue is recorded when the business sells the good |

| How is double-entry book keeping better than single-entry? | if a business is using double-entry accounting, when the business purchases goods they record an increase in inventory along with a decrease in assets at the same time and within the same transaction. it enable accurate calculations and simplify the preparation of financial statements, it also helps to reduce the risk of errors or fraud. Double-entry accounting is required under Generally Accepted Accounting Principles (GAAP). Single-entry accounting is only practical for smaller businesses with low transaction volumes, as it fails to take concepts like inventory into account. A business also can not use single-entry accounting to create certain necessary financial documents, like balance sheets. |

| What is Book value? | In accounting, book value is the value of an asset according to its balance sheet account balance. For assets, the value is based on the original cost of the asset less any depreciation, amortization or impairment costs made against the asset. |

| What is Trial balance? | A trial balance is an internal financial statement that lists the adjusted closing balances of all the general ledger accounts contained in the ledger of a business as at a specific date. |

| What is a Discount? | a deduction from the usual cost of something, typically given for prompt or advance payment or to a special category of buyers |

| What is Net cash flow? | Net cash flow is a profitability metric that represents the amount of money produced or lost by a business during a given period. Usually, you can calculate net cash flow by working out the difference between your business’s cash inflows and cash outflows. |

| What is Goodwill? | In accounting, goodwill is an intangible asset recognized when a firm is purchased as a going concern. It reflects the premium that the buyer pays in addition to the net value of its other assets. |